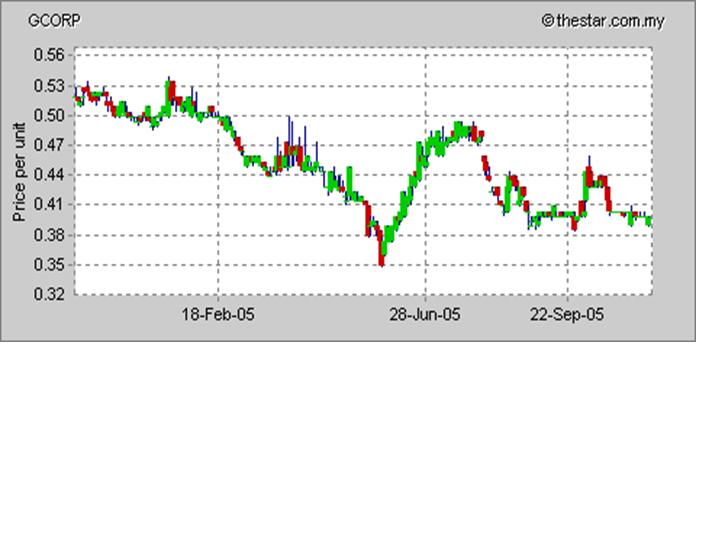

Gcorp @ M0.40

General Corporation Berhad

I am a staunch advocator of the much esteemed Low Keng Huat, so how can I possibly miss out on its grossly undervalued holding company – General Corporation. Several positive catalysts have since transpired and a rerating of the stock seems imminent and we will provide a meticulous breakdown of these determinants in our analysis.

Profile

General Corporation Berhad’s(GCB) principal activity is developing of residential and commercial properties. Other activities include manufacturing of tyres and other rubber products for industrial use, manufacturing of confectionery products, investment in associates, construction of buildings, quarry operations, provision of management services and investment holding. Operations are carried out in Malaysia, Australia, Singapore and other countries.

Balance Scorecard

Half Year 06 FY05 FY04

Net profit M$3,733,000 M$6,137,000 M$10,167,000

EPS M$0.0127 M$0.0207 M$0.0342

Debt/ Equity 0.0490 0.0681 0.1032

Current Ratio 2.13 2.17 2.00

Share Information

Date 31.01.05 29.07.05

Price M$0.51 M$0.47

P/E 24.6x 22.7x

Dividend Yield 5.4%

Adjusted NTA 1.338

Positive Catalysts- Cessation of loss-making Rubber and Confectionary Division

GCorp’s rubber products division, represented by Fung Keong Rubber Manufactory, has shut down its loss-making manufacturing activities since early this year. Moreover, its confectionery division whose products are marketed in Australia under the Simpsons, Charlie and Uncle Bills brand names have been plagued by high commodity prices and limited operating efficiency compared to global brands such as Cadbury, Hershey and Nestle.

Henceforth, for the past few years, GCB's rubber products division and confectionery business have endured acute haemorrhage. Thank god! The drain on the coffers has now been arrested with the cessation of Fung Keong Rubber Manufacturing, Vredestein FKR and English Style Confectionary.

However, the liquidation of both the rubber products and confectionery divisions will only benignly elevated its financial results from 2006 onwards and a net loss of about RM5.1 million will still materialize for FY06.

The Goose that lays golden eggs

Gcorp’s associate Low Keng Huat is shedding its mammoth baggage through its aggressive rationalization and divestment plans in order to capitalize on its core competency of property development(Refer to my earlier article to get a good grasp of LKH).

The causes for rejoice are aplenty -- the property market in Singapore has hit rock bottom and LKH is poised to book some hefty gains with the divestment of several non-core assets. Besides, LKH forging a strategic partnership with UOL/UIC by leveraging on each other comparative advantage will put both parties in good stead in time to come. The tie-up with Wee Cho Yaw is a match made in heaven as Gcorp will assist UOL/UIC to break into the Malaysian property scene. In return, LKH can tap onto UOL’s brandname/expertise and UOB’s financial clout to offer innovative financing for its home buyers.

The beauty of geographical diversification is finally bearing fruit -- with Malaysia experiencing a softening of its property sector, adverse operating conditions is bound to delicately dent its operating figures which will be opportunely offset by favourable operating results from its Singapore division.

According to my estimates, LKH is expected to register a profit of at least S$33.6 million for its 2nd half FY06, translating into M$36 million filtering down into Gcorp’s bottomline. However, its loss making divisions will most likely trim the gains to M$30millions, evolving into an alluring EPS of M$0.114 and undemanding PE of 3.5x at the current price level of M$0.4.

Over the medium term, with new launches in the pipeline commanding an estimated gross value of RM720 million, Gcorp is poised for a rerating by the investment community.

A blemish that smudged the masterpiece

Low Keng Huat outstanding shares is 120,953,000

General Corp owns 48.6% of Low Keng Huat

Net asset quoted outside Malaysia -- M72,773,000 (Low Keng Huat) Item 15 of AR

Book Value of Low Keng Huat – 72,773,000 + 37,110,000/(48.6% x 120,953,000) = M$1.87/share = S$0.841

In item 15 of the AR, the market value of quoted shares (Low Keng Huat) is M$58,366,000, whereas the net book value of these shares in GCorp’s balance sheet is M$139,080,000 indicating (M$139,080,000 - M$58,366,000) /297,084,626 = M$0.272 /share of its NTA is at best “illusionary” and not realizable in the immediate future.

Interestingly, General Corp. adopt an extremely aggressive stance of accounting(far more superior to marked to market valuation) that booked its associates’ interests at cost plus retained profits. At the time of inception, Low Keng Huat is trading at a mere S$0.43, yet the net book value of these shares is lodged at an astronomical high of $0.841 which will only sky rocketed further as long as LKH stays in the black. Retained profit is mere form and short on substance as a single bad investment decision can wipe out years of cumulative retained profits in the blink of an eyelid.

Burden with these lingering doubts, I made a call to Gcorp, hoping that they could shed some light on the true net book value of LKH. What could be more enlightening than a answer from the horse mouth. Their evasive posture of refusing to provide me with an actual figure confirmed my initial suspicions.

Merits

With its haemorrhage arrested, management is now poised to start afresh from a clean slate and embarked on its next phase of expansion – building up its land bank and zealously growing its bottomline through new property launches. The invigoration of new blood (Low’s descendents) into the management ranks seems to have injected a new lease of life into its business. Taking a cue from LKH”s AR which will smitten every investor who see this writings on the wall “priority was given to improve bottomline and shareholders’ returns rather than increase turnover at the expense of profitability.”

Although NTA was artificially inflated through some incongruous accounting methodology, however, at its adjusted NTA of M$1.338, Gcorp is only trading at a mere 0.30x of its NTA, coupled with a attractive forward PE of 3.5x, all these inherent ingredients primed GCorp for a stratospheric rise to the moon.

posted by Fesserie at 7:55 AM

![]()

0 Comments:

Post a Comment

<< Home